Running a gas station and convenience store today is more than managing fuel sales and, in-store transactions a big part of profitability comes from vendor rebates and promotional allowances.

Yet these income streams are often ignored, not tracked properly or recorded late which creates gaps, in reporting and makes you doubt your numbers.

For convenience store and gas station owners or managers a system to track earnings is very important.

A CFO-led approach brings discipline to capturing rebates and using them strategically to improve margins.

Why Vendor Rebates and Allowances Matter

Vendor rebates and promotional allowances are not just minor adjustments. They are an important and often underutilized part of your revenue model.

They typically include:

- Volume-based purchase incentives

- Promotional display agreements

- Slotting fees and product placement

- Vendor-supported marketing programs

For gas stations and convenience stores, the amounts of money they make from things, like beverages, tobacco and packaged goods, can really affect how profit they get in the end.

Many operators do not have an idea of their income until the end of the month or sometimes even later when it comes to the income of the operators.

Snippet Answer: What Are Vendor Rebates in Convenience Stores?

Vendor rebates are incentives that suppliers pay to you based on how much you buy from them. They are a key part of your true revenue and profitability when you track vendor rebates correctly.

The Hidden Problem: Inconsistent Tracking

Most gas stations and convenience store operators use vendor statements, emails, or manual logs to track rebates.

The challenge is not a lack of information. It is the absence of structure and consistency.

Common issues include:

- Recording rebates only when cash is received instead of when earned

- Missing or incomplete documentation for vendor agreements

- No reconciliation between expected and actual payments

- Limited visibility across multiple locations

Whether you operate a single location or are evaluating a gas station and convenience store for sale in Florida, NJ, or Virginia, this lack of structure leads to unreliable financial reporting.

Types of Vendor Income You Should Track

A well-designed system separates each type of vendor’s income clearly, so you understand where your profitability is coming from.

Volume Rebates

These are tied to purchase levels over a specific period.

They require:

- Monitoring purchase thresholds

- Tracking vendor agreements

- Matching expected rebates with actual payments

Promotional Allowances

These relate to in-store promotions, displays, or marketing campaigns.

You need visibility into:

- Campaign timelines

- Vendor commitments

- Performance requirements

Slotting and Placement Fees

Vendors often pay for premium shelf space or visibility.

Tracking these separately helps you evaluate category-level profitability more accurately.

For operators managing convenience stores and gas stations, this level of clarity provides a much stronger foundation for decision-making.

Why Traditional Accounting Falls Short

Standard bookkeeping approaches often fail to capture vendor income accurately.

Typical gaps include:

- Recording rebates only when cash is received

- Treating rebates as expense reductions instead of revenue

- Lack of accrual-based tracking

- Limited audit trail

The result is distorted margins and incomplete financial visibility.

Operators using structured bookkeeping and financial statements of preparation gain a much clearer and more reliable view of performance.

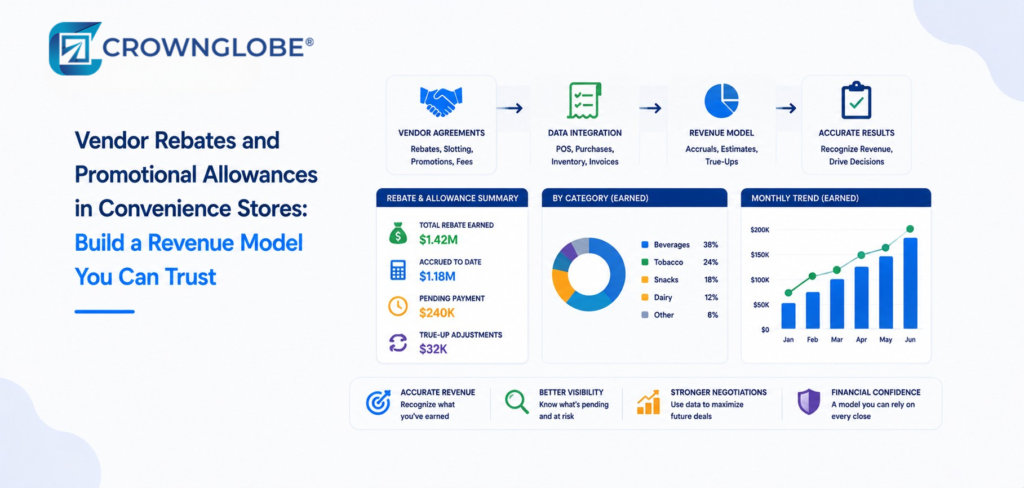

A CFO Approach to Building a Reliable Revenue Model

A CFO does not treat rebates as occasional or unpredictable income. Instead, they are managed as structured and measurable revenue streams.

Accrual-Based Recognition

Rebates should be recorded when they are earned, not when payment is received.

This provides:

- Accurate monthly reporting

- Better visibility into margins

- More reliable forecasting

Agreement Tracking and Validation

Every vendor agreement should be documented and actively tracked.

This includes:

- Expected rebate amounts

- Payment timelines

- Performance conditions

Without this structure it’s hard to confirm if you are getting the value you deserve.

Reconciliation and Control

A strong system regularly compares:

- Expected rebate amounts

- Vendor statements

- Actual payments received

This helps identify:

- Missing payments

- Underpaid rebates

- Timing differences

For operators reviewing a gas station and convenience store for sale in Pennsylvania, this level of control is essential for proper due diligence.

Using Power BI for Rebate Visibility

Manual tracking quickly becomes inefficient as your operations grow.

With Power BI visualization, you can build dashboards that clearly show:

- Rebates by vendor and product category

- Expected versus received income

- Trends over time

- Performance across locations

When finance automation and data work together, your data gets updated away and you can see the latest information, in real time.

This is especially valuable for a chain of convenience stores and gas stations, where small gaps across locations can add up to amounts.

Multi-Location Complexity and Opportunity

As you expand, vendor rebates become more complex, but also more valuable.

You need to:

- Consolidate vendor agreements across locations

- Track performance at the store level

- Benchmark rebate income across your portfolio

This creates opportunities for companies to negotiate terms and improve the profitability of the companies.

For people who run convenience stores and gas stations in places, like Texas, New Jersey or Virginia, it is really important to have a view of what is going on at all the locations.

Compliance and Reporting Considerations

Vendor rebates must be handled correctly for both financial reporting and compliance.

You should ensure:

- Proper classification aligned with NAICS code for gas station and convenience store

- Accurate reporting using the activity code for gas station and convenience store

- Consistent documentation for audit readiness

- Clear treatment of vendor income when assessing the difference between gas station and convenience store revenue streams for reporting purposes

Accurate reporting also supports requirements such as Florida gas station and convenience store insurance and lender reporting standards.

Tax Considerations and IRS Perspective

From a tax standpoint, rebates and allowances can directly affect how income and expenses are reported.

Important considerations include:

- Whether rebates are treated as income or cost adjustments

- Timing of recognition for tax purposes

- Proper documentation to support reporting

Accurate tracking helps you:

- Avoid underreporting income

- Capture all eligible deductions

- Maintain clean and audit-ready records

You can get information by looking at Maximizing Tax Deductions and Credits for Retail Stores and Tax Planning Strategies, for Retail Stores.

Common Mistakes That Reduce Rebate Income

Many operators unintentionally lose revenue due to:

- Poor tracking of vendor agreements

- Lack of reconciliation between expected and received payments

- Overreliance on manual spreadsheets

- Inconsistent income recognition

- Missing promotional conditions

These issues are particularly common among operators reviewing gas stations and convenience stores for sale without a structured financial system in place.

Practical Workflow: Rebate Tracking System

A structured workflow typically includes:

Step 1: Capture Agreements

Document all vendor rebate and promotional terms

Step 2: Track Earned Income

Record rebates as they are earned

Step 3: Reconcile Payments

Match expected amounts with actual receipts

Step 4: Monitor Trends

Use dashboards to track performance over time

Step 5: Report Accurately

Include rebates in financial statements consistently

This approach creates a reliable and transparent revenue model.

How Crownglobe Helps Convenience Store Owners

Crownglobe supports gas station and convenience store owners with systems designed to improve financial clarity and control.

This includes:

- Bookkeeping and outsourced accounting

- Virtual CFO services

- Finance automation

- Power BI dashboards

- Payroll processing and compliance

- Year-end financial checkups

The focus is straightforward: helping you capture every dollar you earn and turn it into actionable financial insight.

Conclusion

Vendor rebates and promotional allowances are not secondary income streams. Your profitability has a part that people often do not use.

For a gas station and convenience store, a system to track income helps create clarity and control over their finances.

You get a revenue model with a CFO in charge which helps you make good decisions and have long-term growth, with the company’s revenue.

FAQ Section

How do vendor rebates work in convenience stores?

They are incentives paid by suppliers based on purchase volume, promotions, or product placement agreements.

Should rebates be recorded as revenue or expense reduction?

It depends on accounting treatment, but they should always be tracked consistently to reflect true profitability.

How can I ensure I receive all vendor rebates?

By tracking agreements carefully, reconciling expected and received amounts, and using automated systems.

Do rebates impact tax reporting?

Yes. Proper classification and timing are essential for accurate tax reporting.

Can dashboards help track vendor income?

Yes. Dashboards provide real-time visibility and improve both accuracy and decision-making.