There is no best way to handle bookkeeping for a real estate brokerage. It really depends on how transactions you do what kind of reports you need and what your goals are. You should also think about what resources you have, inside your company.

Ignore warning signs, like delays and inconsistent reports at your own risk it is time to reassess your current brokerage setup.

Strong real estate bookkeeping is far more than an administrative responsibility. The financial information forms the foundation of financial reporting, tax compliance, payroll support and sound business decision-making for the company’s financial information.

For many growing brokerages, the real question is not whether bookkeeping is being completed. The main thing to think about is if your reporting process gives you the clarity and visibility needed to run and scale the business.

Why This Decision Matters More as Your Brokerage Grows

Most brokerages start with relatively simple financial operations.

A small team of agents.

Manageable transaction volumes.

Basic accounting software.

Bookkeeping handled by an owner, office manager, or internal staff member.

In many cases, that structure works well in the early years.

Growth changes the equation.

As brokerages expand, financial processes become more demanding.

Commission plans become more complex.

Additional teams join the organization.

Payroll responsibilities increase.

Technology expenses grow.

New business entities may be created.

Without strong financial controls, reporting quality often begins to suffer.

This is where professional real estate accounting becomes increasingly valuable. Whether your brokerage relies on internal staff, a dedicated accountant for real estate, or specialized real estate bookkeeping software, accurate financial reporting becomes essential as transaction volume and operational complexity increase.

Reliable financial reporting helps brokerage owners:

- Understand profitability by office, team, or division

- Monitor commission expenses accurately

- Track cash flow trends

- Produce dependable financial statements

- Support tax compliance requirements

- Make better forecasting and planning decisions

When reporting quality declines, decision-making becomes more reactive and far less effective.

Signs Your Current Bookkeeping Process May Be Falling Behind

Many brokerage owners do not recognize reporting problems until the tax season arrives a lender requests statements or brokerage owners have cash flow questions, about their brokerage.

In reality warning signs usually appear earlier.

Month-End Reporting Takes Too Long

A healthy accounting process should produce timely and reliable reports.

If it takes six to eight weeks after month-end to receive statements the financial statements reporting process of the financial statements may already be struggling with the financial statements.

Business owners need the current information to make good decisions because old numbers from several weeks ago are not very useful, to the owners.

Delayed reporting often points to:

- Capacity constraints within the accounting function

- Inefficient bookkeeping processes

- Unresolved reconciliation issues

- Limited accounting oversight

Financial Statements Frequently Change

If reports require repeated revisions, confidence in the numbers naturally begins to erode.

Common issues include:

- Duplicate transactions

- Incorrect expense classifications

- Missing commission entries

- Unreconciled accounts

Accurate reporting starts with disciplined bookkeeping for real estate businesses and consistent review procedures throughout the month. Strong property accounting practices and reliable property management bookkeeping processes help ensure commissions, expenses, and operational reporting remain accurate.

Commission Reporting Is Difficult to Verify

Commission tracking remains one of the most common challenges for growing brokerages.

Questions such as these should be easy to answer at any point in time:

- What commissions are currently owed?

- Which commissions have already been paid?

- Which agents generate the strongest margins?

- Which transactions remain open?

If your team spends hours every month pulling information from spreadsheets or systems then the reporting processes, for your team need improvement.

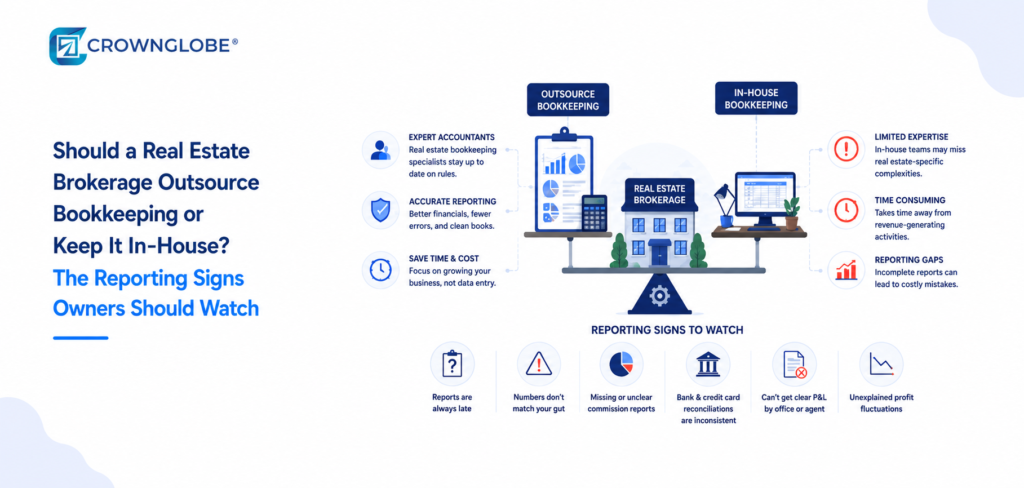

The Advantages of Keeping Bookkeeping In-House

For some brokerages, maintaining an internal accounting team continues to be the right choice.

Benefits of an Internal Team

An in-house accounting function can provide:

- Immediate access to financial records

- Direct communication with operational staff

- Strong familiarity with daily business activities

- Faster coordination with leadership

Brokerages with experienced accounting personnel and established processes may find this model works well.

Potential Challenges

However, internal teams can also create challenges as the organization grows.

Common concerns include:

- Employee turnover

- Limited specialized accounting expertise

- Difficulty scaling workloads

- Heavy reliance on a single employee

- Higher payroll and benefits costs

Many brokerage owners eventually discover that bookkeeping responsibilities have become larger and more complex than their internal structure can efficiently support.

The Advantages of Outsourced Bookkeeping

Outsourced bookkeeping has become increasingly common among growing real estate firms.

The reason is simple. Owners want stronger reporting, improved controls, and access to professionals who understand the financial complexities of the real estate industry.

Access to Specialized Real Estate Accounting Experience

Real estate businesses face accounting challenges that differ from many other industries.

These often include:

- Complex commission structures

- Escrow-related transactions

- Independent contractor payments

- Property management revenue streams

- Multi-entity reporting requirements

An experienced real estate accountant understands these nuances and can often identify reporting issues before they become larger financial problems. This specialized expertise is one reason many firms seek support from professionals experienced in accounting for real estate businesses and brokerage operations.

More Consistent Financial Reporting

Professional accounting providers typically follow structured processes for:

- Account reconciliations

- Financial statement preparation

- Month-end close procedures

- Documentation management

- Compliance support

Consistency creates confidence in the numbers.

And confidence in the numbers leads to better business decisions.

Scalability Without Adding Headcount

As the number of transactions increases the amount of accounting work also increases.

Outsourced support usually scales more efficiently than hiring and training new employees.

That flexibility is one reason many brokerages move toward outsourced accounting and remote accounting solutions as they expand.

Questions Every Brokerage Owner Should Ask

You need to look at the quality of your bookkeeping and reporting before you decide what to do with your bookkeeping.

Are Financial Statements Available Every Month?

Timely financial reporting is essential for management.

If reports are regularly delayed, owners lose visibility into business performance.

Many growing firms benefit from professional financial statements of preparation support to ensure reports are delivered accurately and on schedule.

Are Bank Accounts Fully Reconciled?

Unreconciled accounts are one of the most common sources of reporting errors.

Every balance sheet account should be reviewed regularly and supported by proper documentation.

Is Bookkeeping Pulling Leadership Away From Revenue Activities?

Brokerage owners create value by growing the business, recruiting agents, building relationships, and improving operations.

If leadership is spending excessive time correcting bookkeeping issues, it may be a sign that current processes are no longer serving the business effectively.

Are You Confident in Tax and Compliance Reporting?

The IRS continues to emphasize the importance of accurate recordkeeping.

Weak bookkeeping processes can create challenges involving:

- Payroll reporting

- Independent contractor reporting

- Tax return preparation

- Financial statement accuracy

Strong accounting practices help reduce the risk of problems, with rules and improve the confidence people have in the reports all year round.

Technology Alone Is Not the Solution

Many brokerage owners assume that implementing new software will automatically solve reporting issues.

Technology certainly plays an important role.

Today’s real estate accounting software, QuickBooks for realtors, bookkeeping software for real estate agents, and other specialized platforms can streamline processes, improve reporting, and reduce manual work.

However, software does not replace accounting expertise.

Even the best real estate business accounting software, accounting software for real estate investors, or best accounting software for realtors depends on:

- Proper setup

- Consistent reconciliations

- Accurate transaction coding

- Ongoing oversight

Technology works best when it has accounting processes and financial leaders who know what they are doing.

When Outsourcing Makes the Most Sense

Every brokerage is different, but outsourcing often becomes an attractive option when:

- Transaction volume is growing quickly

- Financial statements are consistently delayed

- Reporting errors occur regularly

- Multiple entities must be managed

- Internal staff are stretched too thin

- Leadership lacks clear visibility into financial performance

At this stage, many firms seek professional bookkeeping, catch up bookkeeping, or virtual CFO support to improve reporting quality and strengthen financial visibility. This is particularly common among growing firms that require bookkeeping for real estate brokers and more sophisticated financial reporting capabilities.

Brokerages responsible for trust account management may also benefit from reviewing our guide on How to Manage Trust Accounts and Escrow Funds in Real Estate Agencies, which explores best practices for maintaining stronger financial controls.

Likewise, firms facing profitability concerns may find value in Why Real Estate Investors in Dallas Lose Profit Without Strong Accounting Systems, which highlights how reporting weaknesses can quietly affect financial performance over time.

A Practical Evaluation Checklist

If you answer “yes” to two or more of the questions below, it may be worth evaluating whether outsourced support would strengthen your accounting function.

Reporting Questions

- Are financial reports consistently late?

- Are account reconciliations incomplete?

- Do reports frequently require corrections?

- Is commission reporting difficult to verify?

Operational Questions

- Is bookkeeping consuming too much management time?

- Is growth creating reporting challenges?

- Has staff turnover affected accounting quality?

Strategic Questions

- Do you lack visibility in profitability?

- Are forecasting efforts unreliable?

- Is decision-making becoming more reactive than proactive?

These are often signs that the accounting processes need to be looked at before they start to affect the growth and profitability of the company.

Conclusion

The decision to outsource bookkeeping or keep it in-house should never be based on cost alone.

The more important consideration is reporting quality.

As brokerages grow, the financial complexity of the brokerages naturally. The brokerages need better processes to manage the profitability of the brokerages and the compliance of the brokerages.

Strong real estate bookkeeping and estate accounting and financial reporting system is very important for brokerage owners to make good decisions and build a stronger business.

Whether that support, from a team or an outsourced partner should give your brokerage timely and accurate financial information so that your brokerage can operate with confidence and clarity.

FAQ Section

Should a small real estate brokerage outsource bookkeeping?

Not necessarily. Smaller brokerages with relatively straightforward operations can often manage bookkeeping internally. However, owners should regularly assess reporting quality and workload as the business grows.

When should a brokerage consider outsourced accounting?

Many brokerages explore outsourcing when reporting becomes delayed, transaction volume increases, multiple entities are involved, or internal resources struggle to keep pace with growth.

Is outsourced bookkeeping more cost-effective than hiring internally?

It depends on the organization’s needs. Many firms find outsourcing provides access to experienced accounting professionals without the costs associated with hiring, training, and managing additional employees.

What reports should a brokerage review monthly?

At a minimum, brokerage owners should review the Profit and Loss Statement, Balance Sheet, Cash Flow Statement, commission reports, and key performance indicators relevant to the business.

Can software replace a bookkeeper?

No. Software improves efficiency, but accurate bookkeeping still requires human oversight, reconciliations, review procedures, and accounting expertise.