At CROWNGLOBE, we help many small businesses manage their taxation. During the consultation stage, we often find one thing common in almost each of these Small Businesses: They pay a lot more taxes than they have to. There are a lot of deductions and credits available to them that can minimize their tax burden. But these businesses either don’t know about these benefits or don’t understand the complexities involved. One benefit that the IRS offers to such businesses is the depreciation of their assets. As many small businesses don’t know how to use this to their benefit, we decided to develop a blog that can help them understand it. So, let’s begin.

What is Depreciation?

Depreciation is a method that businesses use to allocate the cost of a tangible asset over its useful life. The Internal Revenue Service (IRS) allows this practice, so companies can deduct a portion of the asset’s cost each year. They can do this until they have fully recovered their value. This accounting process reflects the asset’s wear and tear, decay, or obsolescence over time. In short, depreciation indicates the decreasing value of these assets. Businesses leverage depreciation to gradually get back the purchasing cost of items such as vehicles or office equipment. This can help minimize their tax liabilities.

However, certain conditions make an asset qualify for depreciation. Let’s take a look at these conditions:

Ownership: The business claiming depreciation must own the asset. Even if a loan finances the purchase, the business can depreciate the asset because it holds ownership.

Business Use: The asset must be used for business or for generating income. The business can only claim depreciation for the percentage of the asset's use that applies to business activities. Assets used exclusively for personal purposes do not qualify for depreciation. (for e.g. personal vehicle)

Service Duration: The asset must have more than one year of useful life. Items with a shorter lifespan, such as office supplies, are not eligible for depreciation.

Useful Life: The asset must have a measurable life expectancy, meaning it will deteriorate, wear out, become outdated, or lose value due to natural causes.

Businesses can depreciate a wide range of real property assets, including buildings, machinery, office furniture, equipment, and vehicles. However, the IRS does not allow land depreciation for obvious reasons! The value of land generally does not depreciate; instead, it increases.

Businesses can also claim depreciation on some intangible assets, such as purchased computer software, copyrights, and patents. These assets are subject to amortization over their economic lives.

However, some exceptions prevent depreciation:

Businesses cannot depreciate items they use and dispose of within one year.

They must not claim depreciation on equipment to make capital improvements; instead, these costs increase the asset's basis.

Amortization, not depreciation, applies to Section 197 intangibles, often associated with business acquisitions after August 10, 1993, including goodwill and other intangibles.

Restrictions or disqualifications apply to assets owned by related parties as per IRS guidelines.

Overall, there are many ifs and buts when it comes to taking advantage of depreciation. So, it’s always better to consult a professional before taking any step. Now, let’s come to our core question: What are the tax benefits of Depreciation?

How can Depreciation Reduce your tax burden?

Reduced Taxable Income

Depreciation allows a business to allocate the cost of an asset over its useful life instead of taking the full expense in the year of purchase. As the expense is distributed gradually, it can help reduce the taxable income reported each year, according to the IRS.

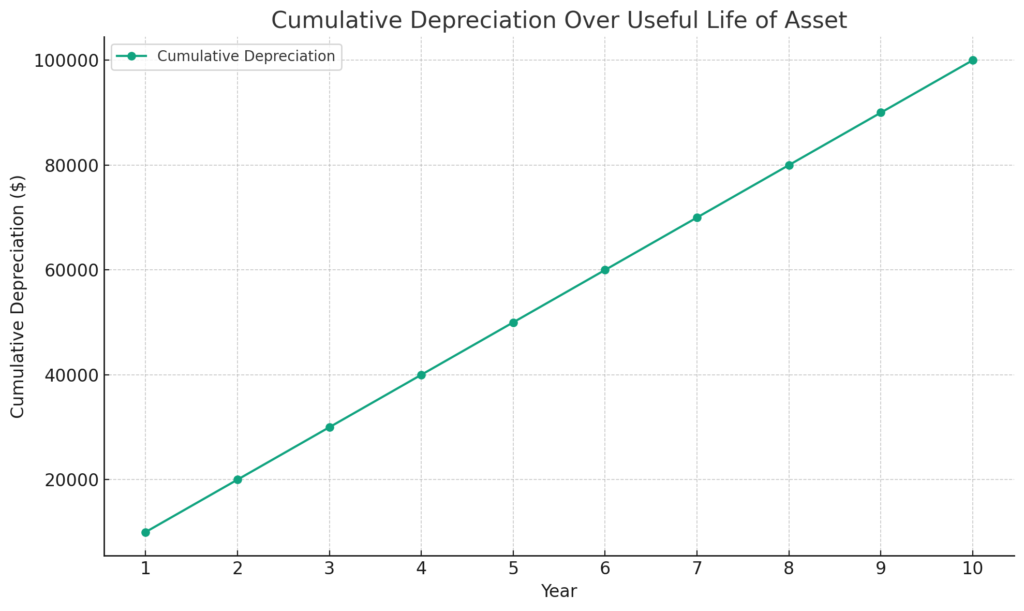

Let’s take an example of a company that purchases equipment for $100,000 with a useful life of 10 years. Now, instead of taking a significant financial hit in year one, the business can spread out the cost. So, they can deduct $10,000 each year as depreciation expense. As per the IRS Publication 946 (2023), the maximum Section 179 expense deduction for tax years beginning in 2024 is $1,220,000, with a phase-out threshold starting at $3,050,000 in property purchases. So, this provision directly reduces the amount of income subject to tax. This provides a better opportunity to reduce the tax and save money.

Improved Cash Flow

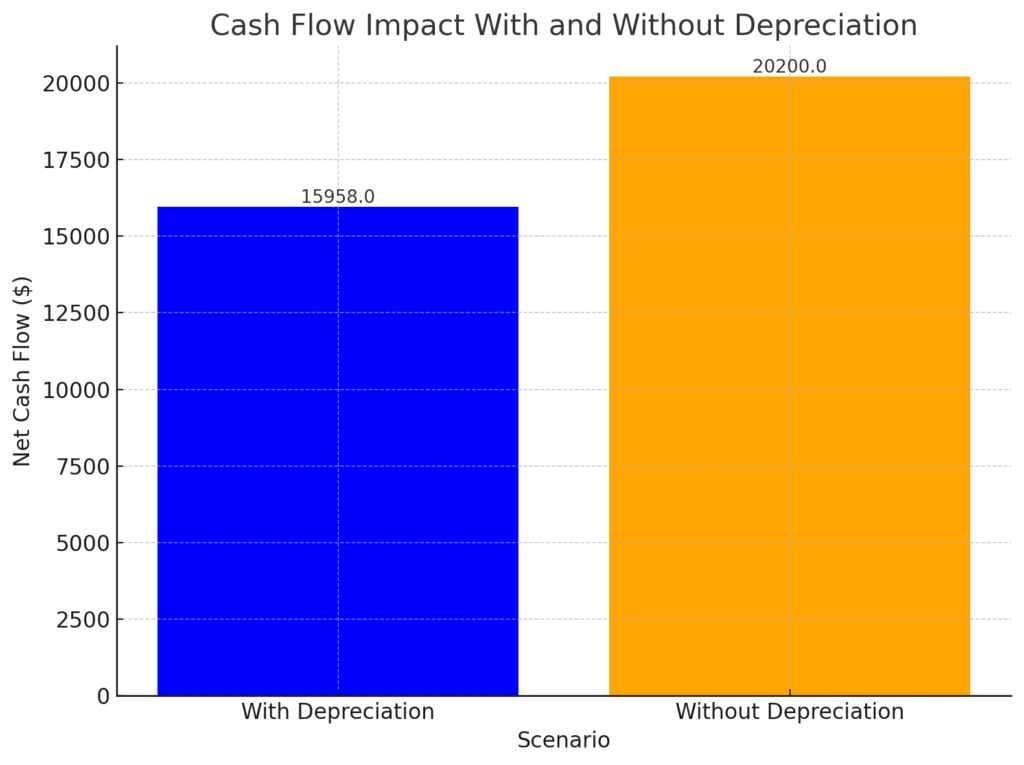

The direct impact of reducing taxable income through depreciation is the improvement of a company’s cash flow. Cash flow is the lifeblood of any business, and that’s where the depreciation can come to your rescue. It can help you conserve a lot of cash. According to IRS guidelines, vehicles used in business and placed in service in 2023, for instance, the total Section 179 and depreciation deduction can be $20,200 if the special depreciation allowance applies.

Once you have preserved more cash, you can reinvest it in your core business and enjoy better growth. You can use that fund to expand business operations, hire additional staff, or increase research and development efforts—all this without impacting the business’s day-to-day operational funds.

Investment Incentive

Depreciation also acts as an incentive for investment in new property and equipment. The Tax Cuts and Jobs Act, as outlined in the IRS’s comparison for businesses. This has altered depreciation rules after introducing the additional first-year depreciation deduction (bonus depreciation). For qualifying property, this bonus depreciation allows businesses to immediately deduct a substantial portion of the purchase price before the standard depreciation schedule begins. This is an excellent benefit. Per the latest IRS guidelines, the special depreciation allowance is 60% for certain qualified property acquired after September 27, 2017, and placed in service after December 31, 2023, and before January 1, 2025. This upfront deduction can significantly lower the initial cost barrier. This deduction encourages businesses to invest in assets that contribute to their growth. The best part? The incentives do not end with the immediate year’s tax return. The depreciation deductions can yield tax benefits that extend into future years for businesses. For example, Publication 527 (2023) indicates that rental property owners can deduct a certain percentage of an asset’s cost annually. According to the General Depreciation System (GDS), this period can extend up to 27.5 years for residential property.

Minimize Your Tax with Professionals

Depreciation offers small businesses an excellent opportunity to minimize their tax burden. However, the list of requirements and what exactly you can claim are a bit complex. So, the best approach is to consult professionals like CROWNGLOBE, specializing in the matter. So, if you are a small business owner looking for options to slash your taxes, we can help you with that. Get in touch today for more details.

Admin