Retirement Planning: A Deep Dive into Securing Your Future

Retirement planning is more than just saving money; it’s about strategizing for a future where you can enjoy life without financial worries. This extensive guide aims to cover all corners of retirement planning, ensuring that you’re more than ready to step into your golden years with confidence and security when the time comes.

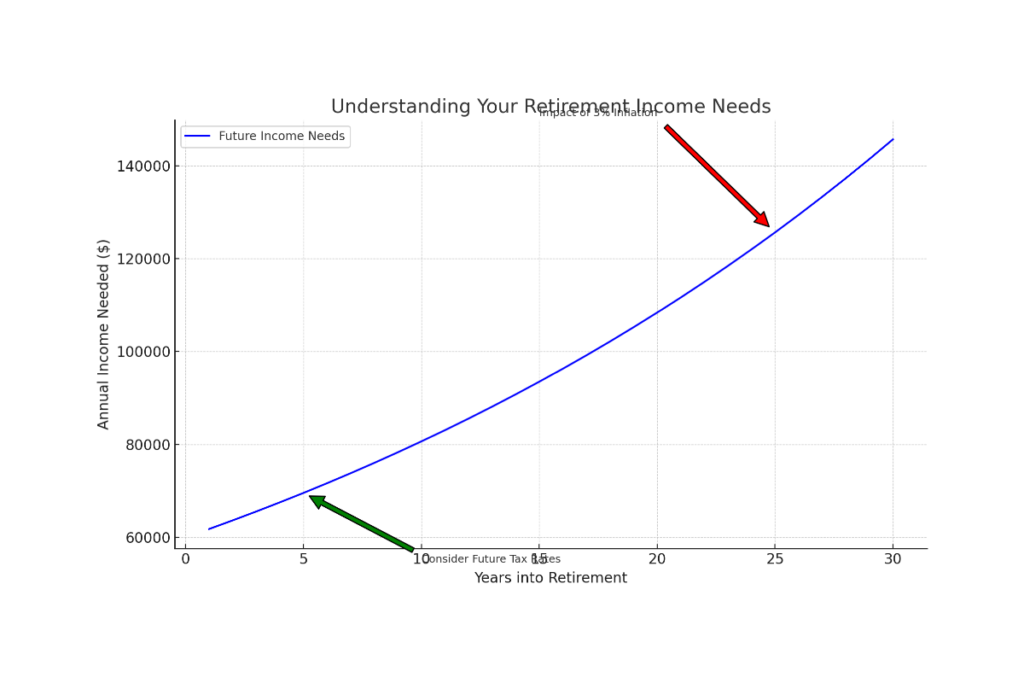

Understanding Your Retirement Income Needs

The foundation of retirement planning lies in understanding how much income you’ll need to maintain your desired lifestyle. It’s a complex calculation involving your current living expenses, anticipated inflation rates, and expected future tax scenarios.

Inflation’s Impact: Inflation significantly affects your purchasing power, making today’s dollars worth less in the future. Planning for inflation is critical, and using an inflation rate of 3% for projections can help you adjust your savings strategy to preserve your purchasing power over time.

Future Tax Rates: Anticipate changes in tax rates, especially if you plan to retire in a different state. Your retirement income needs should consider these potential tax liabilities to avoid any surprises.

The Role of Individual Retirement Arrangements (IRAs)

IRAs are a cornerstone of retirement planning, offering tax-advantaged savings options. The choice between a traditional IRA and a Roth IRA is pivotal and should be based on your current tax situation and anticipated retirement tax bracket.

Traditional IRA: Contributions to a traditional IRA may be fully or partially tax-deductible depending on your income, filing status, and whether a workplace retirement plan covers you. The tax deduction can provide immediate tax benefits, with taxes on earnings deferred until withdrawals, taxed as ordinary income. For 2023, individuals can contribute up to $6,500 or $7,500 for those aged 50 or over. Importantly, contributions to a traditional IRA can be made past age 70½, allowing for continued retirement savings growth.

Roth IRA: Roth IRA contributions are made with after-tax dollars, meaning there’s no tax deduction at the time of contribution. However, the advantage of a Roth IRA is that both the contributions and the earnings can be withdrawn tax-free in retirement, provided certain conditions are met. The Roth IRA has income limits for eligibility; for instance, in 2023, married couples filing jointly with modified adjusted gross incomes between $218,000 and $228,000 can make reduced contributions, and those with higher incomes are ineligible for direct contributions. However, they may still be able to convert a traditional IRA to a Roth IRA.

Employer-Sponsored Retirement Plans

Employer-sponsored retirement plans, such as 401(k)s, serve as a fundamental method for retirement savings. These plans allow employees to save and invest a portion of their paycheck before taxes are taken out.

Maximizing Contributions: Employees are encouraged to contribute the maximum allowable amount to their 401(k) plans, especially when employers offer matching contributions, which can significantly enhance retirement savings. The vesting schedule is crucial as it dictates when you gain full ownership of these employer-contributed funds.

Diversifying Through ESOPs and NQDC Plans

ESOPs: Employee Stock Ownership Plans provide employees with an ownership interest in the company. While ESOPs can offer substantial financial benefits as the company grows, balancing this investment with other retirement savings is important to mitigate risk.

NQDCs: Nonqualified Deferred Compensation plans allow employees to defer a portion of their income to future years, typically to take advantage of lower tax rates in retirement. However, unlike qualified plans protected by ERISA, NQDC plans are subject to the employer’s credit risk, highlighting the importance of understanding the employer’s financial stability.

Social Security Benefits: Maximizing Your Income

Social Security benefits form a critical part of retirement income. The strategy around when to claim benefits can significantly impact your financial security in retirement.

Strategic Claiming: While you can start receiving Social Security benefits as early as age 62, waiting until full retirement age (FRA) or even until age 70 can significantly increase your monthly benefit. The decision on when to claim should consider your overall financial situation, health, and life expectancy. The Social Security Administration provides various calculators to help estimate your potential benefits at different ages, assisting in this crucial decision-making process.

Contributing Beyond the Basics

Diversifying your saving strategies can significantly impact your financial security in your golden years. Beyond traditional retirement accounts, annuities and plans tailored for self-employed individuals or small business owners, such as SEP and SIMPLE IRAs, offer unique benefits and higher contribution limits. It presents an excellent opportunity for increasing your retirement savings.

Annuities provide a guaranteed income stream in retirement, appealing to those looking for stability and predictability. The tax-deferred growth potential of annuities allows your investments to grow without immediate tax implications, providing a strategic advantage in long-term financial planning.

SEP (Simplified Employee Pension) and SIMPLE (Savings Incentive Match Plan for Employees) IRAs are designed to accommodate the unique needs of self-employed individuals and small business owners. These plans offer more generous contribution limits than traditional and Roth IRAs, enabling significant pre-tax savings and growth potential, which is particularly beneficial for late starters in retirement planning or those looking to catch up.

Navigating IRA Contribution Limits and Strategies

Understanding the intricacies of IRA contribution limits and strategies are essential for maximizing your retirement savings. The IRS sets specific limits on how much can be contributed to IRAs annually, and these limits can have significant implications for your tax situation and retirement planning strategy.

For individuals covered by a workplace retirement plan, the deductibility of traditional IRA contributions is subject to phase-outs based on income levels. As your income increases, the amount you can deduct on your taxes for IRA contributions decreases, potentially affecting your immediate tax benefits.

For Roth IRA contributions, higher earners may find themselves phased out of direct contributions due to income limits. However, a backdoor Roth IRA conversion presents a viable strategy for those still wishing to take advantage of the Roth IRA’s tax-free growth and withdrawals. This involves contributing to a traditional IRA and then converting that contribution to a Roth IRA, navigating the income limits.

Required Minimum Distributions (RMDs) and Tax Implications

Once reaching age 72 (or 73, depending on your birth year as adjusted by recent legislation), account holders must start taking RMDs from their retirement accounts. These mandatory withdrawals have tax implications and are calculated based on the account balance and holder’s life expectancy.

Failing to take the required distribution can result in significant penalties, underscoring the importance of planning for RMDs in your retirement strategy. This planning ensures that your savings are optimized for growth and compliant with tax regulations, avoiding unnecessary penalties and maximizing your income in retirement.

The Power of Early and Consistent Contributions

The benefits of starting your retirement savings early cannot be overstated. Compounding interest profoundly affects the growth of your retirement fund, meaning that even small contributions made early and consistently over time can accumulate into significant savings.

Starting early gives your investments more time to grow, leveraging the power of compounding to increase your retirement fund exponentially. This approach underscores the importance of consistent contributions, regardless of the amount, to ensure steady growth of your retirement savings over time.

Professional Guidance and Personalized Strategies

Retirement planning is a highly personalized process reflecting your financial situation, goals, and needs. Seeking professional guidance can be invaluable in navigating the complexities of retirement planning.

A financial advisor can offer personalized strategies tailored to your unique circumstances, providing expertise on investment choices, tax planning, and adjustments needed over time.

Secure Your Golden Years with Strategic Planning

Remember, the art of retirement planning is in balancing dreams with practicality. Embrace this journey with foresight, and let informed decisions guide each step you take. Your retirement years are a well-deserved chapter of life waiting to be written with joy and peace of mind. Begin this journey today, and step into a future where every sunrise promises a life well-lived and cherished. For any further information, feel free to talk to our experts.

Admin